This is how you can save tax this year

You can use various deductions enlisted in the Income Tax Act to save your income tax liability.

With the end of financial year just around the corner, it is time to save certain amount of taxes by investing in prescribed instruments which are eligible for deductions. Chapter VI-A of the Income-tax Act primarily provides for deduction on certain payments and deduction on certain incomes. Individual taxpayers are eligible to claim these deductions and have a wide range of tax preferences available to them.

Details of deductions which are available to an individual not carrying out any business or profession are as under:

Deduction under section 80C (Maximum upto Rs.1.5 Lakh per annum)

With the end of financial year just around the corner, it is time to save certain amount of taxes by investing in prescribed instruments which are eligible for deductions. Chapter VI-A of the Income-tax Act primarily provides for deduction on certain payments and deduction on certain incomes. Individual taxpayers are eligible to claim these deductions and have a wide range of tax preferences available to them.

Details of deductions which are available to an individual not carrying out any business or profession are as under:

Deduction under section 80C (Maximum upto Rs.1.5 Lakh per annum)

Deduction under section 80CCC The limit of deduction on account of contribution to a pension fund of LIC or IRDA approved insurer is Rs. 1.5 lakhs.

Deduction under section 80CCD

•Under section 80CCD (1) of the Income-tax Act, 1961 if an individual, employed by any other employer (other than the Government), has paid or deposited any amount in a previous year in his account under a notified pension scheme [only the National Pension System (NPS) has been notified by the Ministry of Finance], deduction is allowed up to 10% of his salary.

•Further, with effect from Financial year 2015-16, under section 80CCD (1B) an Individual employee can claim additional deduction up to Rs.50000 by contributing towards NPS.

•Besides, under Section 80CCD(2) employee shall also get deduction in respect of employer's contribution towards his NPS account up to limit of 10% of his salary.

•For this purpose, ‘salary’ includes dearness allowance having regard to the terms of employment but excludes all other allowances or perquisites.

•Limit of deductions under sections 80C, 80CCC and 80CCD(1) is restricted to Rs.1,50,000. Please note that the Individual’s contribution under section 80CCD(1B) and employer’s contribution under section 80CCD(2) is not subject to the overall limit of Rs.1,50,000.

Other Deductions

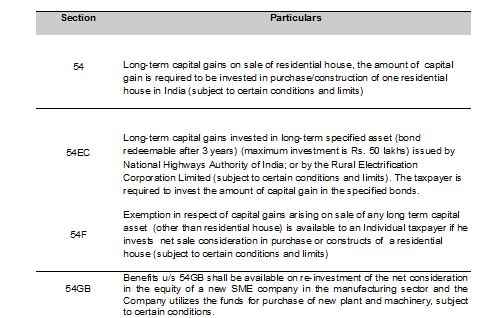

Exemption from Capital Gains Tax

Individual may also earn income by way of capital gain arising upon sale of any long term capital asset on which taxes are applicable at the rates 20% (plus applicable surcharge and education cess). Income tax law allows taxpayer to claim certain exemption from paying such capital gain tax provided certain conditions are fulfilled.

List of exemptions available in relation to Capital Gain is as follows:

The aforesaid deductions are provided under the existing law and the tax payer can opt based on facts, circumstances and their risk appetite.

Happy Investing

Source:Moneycontrol.com

No comments:

Post a Comment